Finance · Story

Kospi Drops 3% as Middle East Strikes Roil Asian Equities

South Korean shares led declines across the region while investors weighed escalating US-Iran tensions and watched for central bank signals from Sintra.

KEY TAKEAWAYS

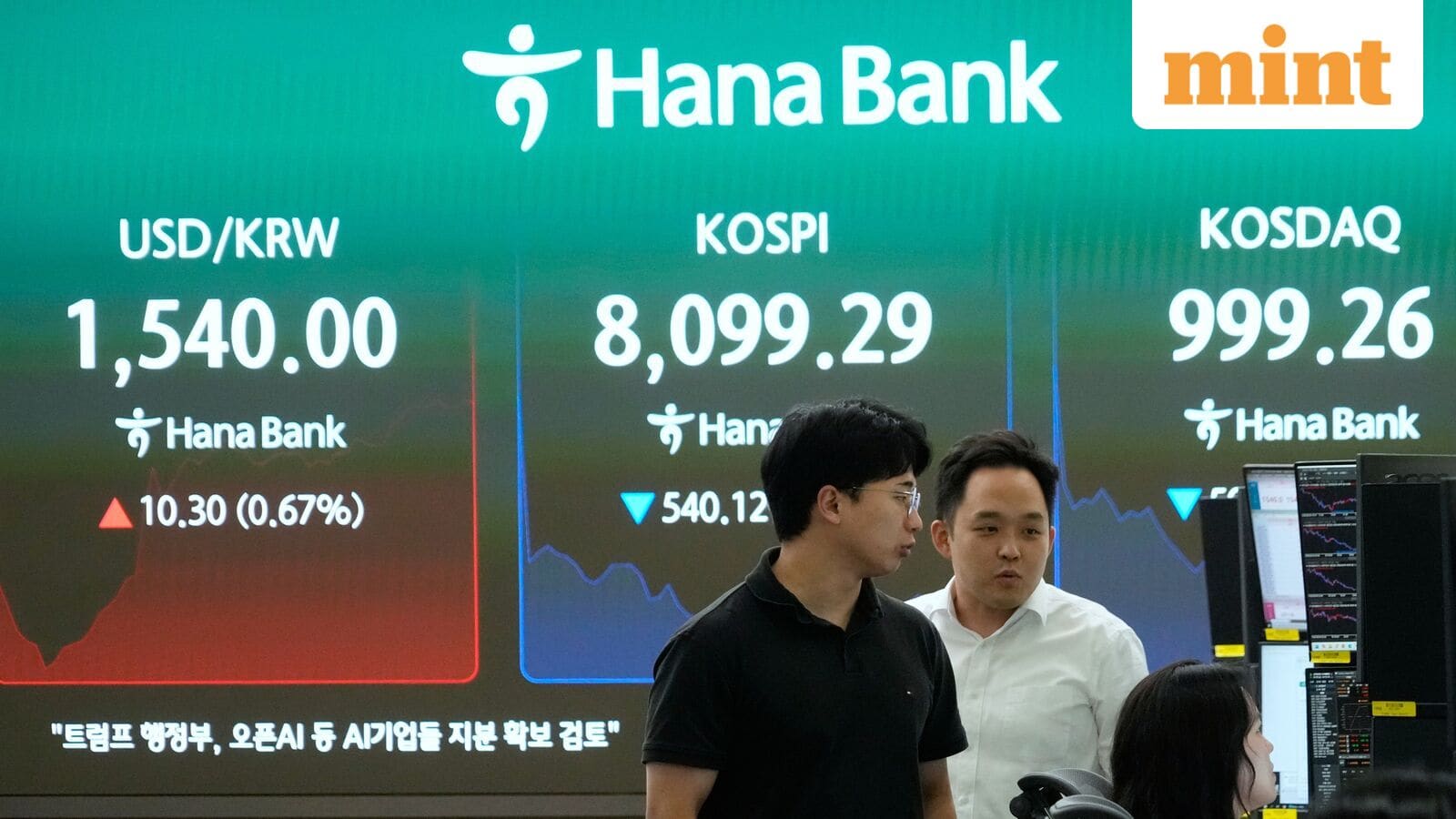

- ·South Korea's Kospi fell 3% at the open on Monday while Japan's Nikkei 225 declined 1%, driven by investor concerns over weekend US strikes on Iranian military targets.

- ·Brent crude surged as much as 1.9% to above $73 per barrel before easing to $72.10 as traders assessed supply risk from the Strait of Hormuz confrontation.

- ·Samsung Electronics and SK Group are expected to announce combined investments exceeding $1.3 trillion over the next decade, according to Korea Economic Daily.

Divergent Moves Across the Region

South Korea's Kospi index fell 3% at the opening bell on Monday, leading losses across Asia as investors absorbed the fallout from weekend military strikes in the Middle East. Japan's Nikkei 225 declined 1%, though the broader Topix index advanced 0.43%. Australia's S&P/ASX 200 edged up 0.41%, while South Korea's small-cap Kosdaq gained 0.97%, defying the broader risk-off mood.

The sharp divergence within markets underscored the selective nature of Monday's selloff. Large-cap indices with heavy exposure to exporters and cyclical sectors bore the brunt of the retreat, while domestic-focused smaller companies held firmer ground.

Weekend Strikes Fuel Risk Aversion

US forces struck Iranian missile storage facilities and coastal radar installations over the weekend following attacks by Tehran on shipping lanes and allied military positions in the Strait of Hormuz. President Donald Trump issued a warning on Truth Social that the United States would respond with overwhelming force if Iran continued hostile actions, stating the country would face annihilation if the conflict escalated further.

Brent crude initially surged 1.9% to trade above $73 per barrel before settling near $72.10 as traders assessed the potential for supply disruptions. The confrontation intensified last Thursday when Iran targeted a container vessel, a ship carrying Qatari crude, and military bases in Kuwait and Bahrain, triggering multiple retaliatory operations by Washington.

The Strait of Hormuz remains a critical chokepoint for global energy flows, with roughly one-fifth of the world's petroleum passing through the narrow waterway. Any prolonged disruption carries the potential to tighten supply and lift prices, particularly as Asian economies remain heavily reliant on Middle Eastern crude imports.

Samsung and SK Group Investment Plans in Focus

Market attention in Seoul centered on anticipated announcements from Samsung Electronics and SK Group, which are expected to unveil large-scale investment commitments alongside new government policy measures. The Korea Economic Daily reported that the two conglomerates could commit more than $1.3 trillion in combined capital expenditure over the next decade, a figure that would represent one of the largest private-sector investment pledges in South Korean history.

The timing of the announcements suggests coordination with Seoul's industrial policy agenda, aimed at bolstering the country's position in semiconductors, batteries, and advanced manufacturing. South Korea has faced mounting pressure to compete with subsidies and incentives offered by the United States, European Union, and China to attract high-tech production capacity.

Investor focus on domestic policy developments provided a partial offset to geopolitical jitters, though the Kospi's steep opening decline indicated that external risk factors dominated sentiment at the start of the week.

Wall Street Rotation Out of Tech

US equity markets closed the prior week on a mixed note, with the S&P 500 and Nasdaq Composite falling nearly 2% and 4.6%, respectively, as investors rotated away from technology stocks. Nvidia and Alphabet each dropped more than 8%, while Meta Platforms, Apple, and Amazon declined over 4%. SpaceX shares tumbled 17%.

The Dow Jones Industrial Average, with its lighter weighting toward technology, gained 0.6% for the week. Merck and Johnson & Johnson led the 30-stock index, advancing 13% and 11.5%, respectively, as defensive and healthcare names attracted inflows.

The rotation marked a continuation of the trend that began earlier in June, with the S&P 500 down 3% for the month and the Nasdaq off more than 6% as of Friday's close. The Dow remained in positive territory, up over 1% for June, highlighting the divergence between growth-heavy and value-oriented benchmarks.

Central Bank Gathering and Labour Data Ahead

Investors are preparing for the annual central banking conference in Sintra, Portugal, where Federal Reserve Chair Kevin Warsh is scheduled to speak. Markets will parse remarks for clues on the Fed's policy trajectory, particularly as economic resilience and sticky inflation have fueled speculation that the central bank could raise interest rates as early as September.

A series of US labour market reports is due this week, culminating in the closely watched nonfarm payrolls release. Strong employment data would bolster the case for tightening, while any signs of cooling could ease pressure on the Fed to act. Asian markets remain sensitive to shifts in US monetary policy, given the region's deep integration into dollar-denominated financing and trade flows.

The combination of geopolitical risk, shifting sectoral dynamics in US equities, and uncertainty around central bank policy has left Asian investors navigating a complex landscape as the second quarter draws to a close. Seoul's policy announcements and energy market developments will likely drive near-term price action across the region.

RELATED STORIES

Indian Equities Face Tepid Open as Middle East Tensions Flare

Priyanka V. Rao · 3 min

Indian Benchmarks Hold Above Key Thresholds as Oil Prices Retreat

Priyanka V. Rao · 3 min

Aditya Infotech Valuation Hits 47x After 427% Rally, Market Share Claims Draw Scrutiny

Priyanka V. Rao · 4 min

ICICI Bank Leads Value Gains as India's Top Banks Weather Mixed Week

Priyanka V. Rao · 4 min

Spot something wrong? Email editor@briefasia.com. We log every correction publicly.