Finance · Story

Foreign Investors Pull Record Sums From India as Global Yields Rise

Higher returns in developed markets and a depreciating rupee have triggered a sharp reversal in capital flows, with nearly $36 billion exiting Indian equities this year alone.

KEY TAKEAWAYS

- ·Foreign investors have pulled nearly $36 billion from Indian equities in 2026 to date, following a $19.5 billion exit in 2025, while the rupee has weakened 12 percent against the dollar over twelve months.

- ·US corporate bonds now yield above 5 percent and European equivalents near 4 percent, both backed by stable currencies, making India's 7.75 percent corporate yield less attractive after accounting for hedging costs and currency volatility.

- ·Japan's ten-year government bond yield has risen to roughly 2.6 percent, reversing yen carry trades and prompting foreign investors to deploy over $100 billion into Japanese equities while withdrawing $38 billion from India in the past year.

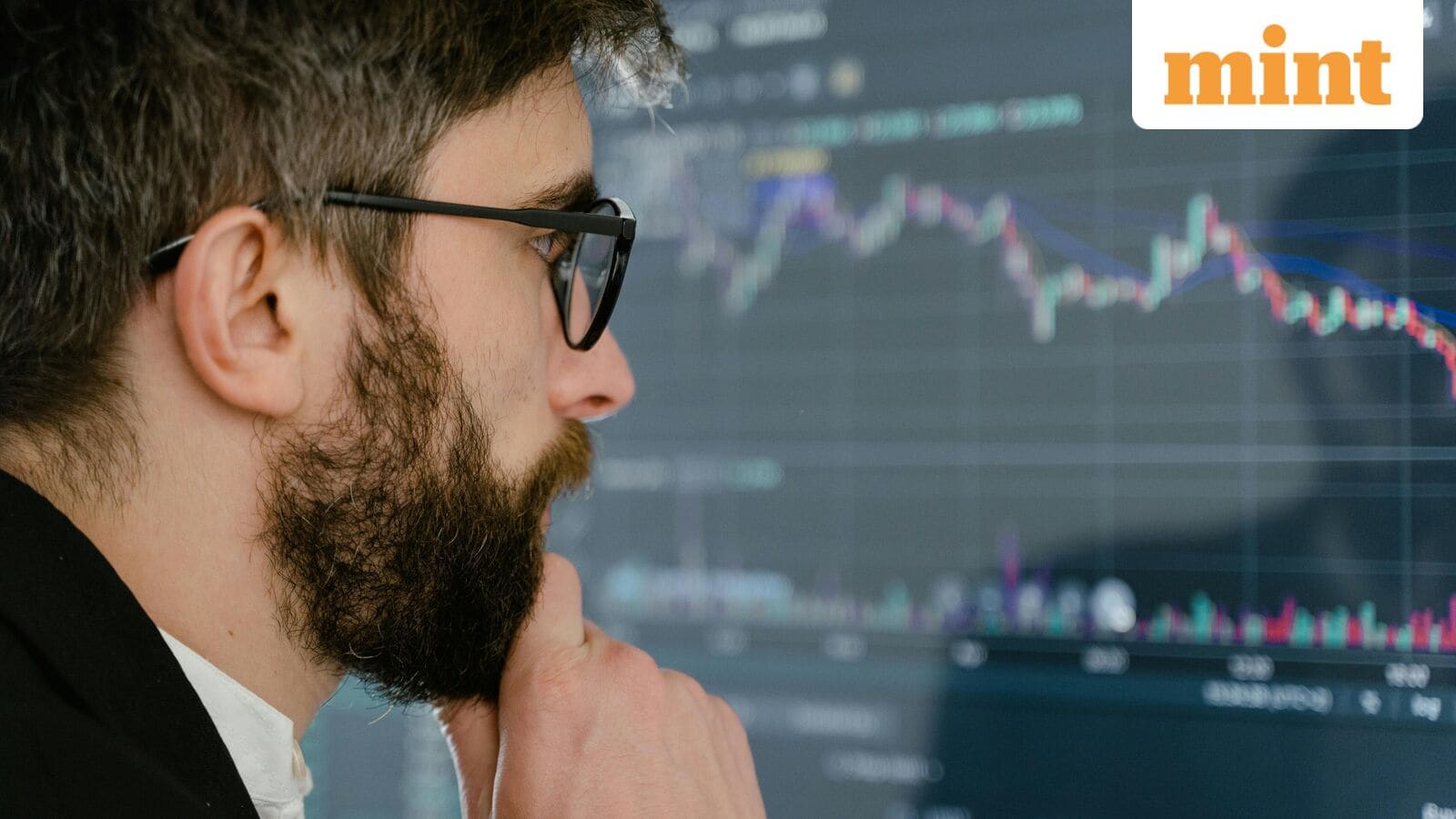

Capital Flight Accelerates

International investors have withdrawn close to $36 billion from Indian equities so far in 2026, building on the $19.5 billion exodus in 2025. The selling pressure marks a dramatic shift from 2024, when net outflows totaled just $390 million, according to data from India's National Securities Depository Limited.

The retreat extends beyond stocks. Debt market inflows collapsed from 107 billion rupees in 2024 to a net outflow of nearly 20 billion rupees in 2025. A modest recovery of 7.7 billion rupees has materialized this year, but the trend remains fragile. Meanwhile, the rupee has depreciated 12 percent over the past twelve months, sliding from 84 to 94 against the dollar.

Yield Differentials Tilt Against Emerging Markets

Corporate bonds in the United States now offer yields exceeding 5 percent, while European equivalents hover near 4 percent. Both are backed by relatively stable currencies and lower hedging costs. By contrast, Indian corporate paper yields around 7.75 percent, a premium that fails to compensate for currency volatility and elevated hedging expenses.

The rupee carries steeper hedging costs than the euro, yen, or Chinese yuan, raising the total expense of forex transactions for foreign portfolio investors. New Delhi has introduced tax incentives on government bonds for non-resident Indians and other foreign buyers, but analysts note the measures cover only a narrow slice of the investment universe.

Japan's Policy Pivot Reverses Carry Trades

A sharp rise in Japanese government bond yields has unwound a decade-long dynamic in which cheap yen funding flowed into higher-yielding Asian assets. Japan's ten-year yield has climbed to approximately 2.6 percent from near-zero levels five years ago, supported by stronger economic growth under a revised policy framework.

Foreign institutional investors have poured more than $100 billion into Japanese equities over the past year while offloading $38 billion from India, according to Geojit Investments Limited. NSDL custody data for May show Japanese holdings in Indian securities down roughly 12 percent year-on-year. Similar declines are visible among investors domiciled in the United States, Singapore, and Mauritius.

Valuation Premium Under Pressure

India's equity market has long commanded a valuation premium relative to regional peers, justified by robust domestic consumption and long-term growth potential. That premium has come under strain as corporate earnings growth slowed during the 2025-26 fiscal year and enthusiasm for artificial intelligence-led expansion remained concentrated in North American technology stocks.

The Nifty 50 index has declined more than 7 percent in March alone, extending losses for a fourth consecutive month. Analysts point to a confluence of factors: subdued profit growth, persistent inflation in services, and geopolitical uncertainty that has kept risk appetite tilted toward developed markets.

Policy Levers and the Path Forward

The Reserve Bank of India and the central government have maintained relatively accommodative domestic interest rates to support local borrowing and investment activity. While that stance has eased funding conditions for Indian corporates, it has widened the gap between local real returns and those available in advanced economies adjusting for risk.

Reversing the outflow trend will require a combination of stronger corporate earnings, deeper integration into global technology supply chains, and fiscal measures that broaden tax incentives beyond sovereign debt. India's anticipated inclusion in the Bloomberg Global Aggregate Index later this year may attract incremental bond inflows, though the scale remains uncertain.

A sustained decline in crude oil prices toward $70 per barrel and easing geopolitical tensions would also support the domestic economy, reduce import costs, and help stabilize the rupee. The Federal Reserve's policy trajectory remains a critical variable; any delay in rate cuts will prolong the yield advantage enjoyed by US Treasuries and dollar-denominated corporate bonds.

Regional Context

Across Asia, central banks face a delicate balancing act. Indonesia and the Philippines have raised rates to defend their currencies, while South Korea has held policy steady despite won weakness. India's challenge is compounded by its large current-account deficit and dependence on portfolio inflows to finance that gap.

Chinese equities have seen modest inflows as Beijing rolls out stimulus measures, but the broader emerging-market complex remains under pressure. Investors are demanding clearer growth narratives and higher risk-adjusted returns before committing fresh capital to the region.

For India, the window to reclaim investor confidence hinges on delivering earnings surprises in the coming quarters and demonstrating that its premium valuation reflects genuine productivity gains rather than past momentum.

RELATED STORIES

India's Equity Markets Show Signs of Recovery Amid Easing Macro Pressures

Priyanka V. Rao · 4 min

Aditya Infotech Valuation Hits 47x After 427% Rally, Market Share Claims Draw Scrutiny

Priyanka V. Rao · 4 min

ICICI Bank Leads Value Gains as India's Top Banks Weather Mixed Week

Priyanka V. Rao · 4 min

ICICI Bank Leads Market Cap Surge Among India's Banking Giants

Priyanka V. Rao · 4 min

Spot something wrong? Email editor@briefasia.com. We log every correction publicly.